[ad_1]

The housing bears have ratcheted up their rhetoric recently, calling for an impeding crash.

It’s not a loopy notion with residence costs clearly unaffordable and mortgage charges not wherever close to 3%.

However typically, a crash or bubble is preceded by artistic financing of some type.

Again in 2006, it was zero down mortgages, said revenue loans, possibility ARMs, and different a lot worse issues.

At this time, the perpetrator is a higher-priced 30-year fastened mortgage, which isn’t all that artistic.

Residence Sellers Can’t Afford to Promote Proper Now

The housing market is tremendous bizarre in the intervening time. Even when owners need to promote, they typically can’t.

Or have little need to because of the unusual mortgage fee setting.

Briefly, most present homeowners have mortgage charges at or beneath 5%, per current HMDA information. And most maintain 30-year fixed-rate mortgages.

Some refer to those residence loans as “golden handcuffs” as a result of they lure owners, but in addition provide one thing of worth.

The problem is these owners can’t transfer as a result of you possibly can’t take your mortgage with you (mortgage disruptors are you listening?).

Let’s contemplate a house owner who bought a property in 2018 for $500,000 after which refinanced in 2021 when the 30-year fastened was sub-3%.

We’ll fake their property is now valued at $700,000, and their mortgage quantity is simply over $360,000.

Their month-to-month principal and curiosity fee is about $1,550. What a steal.

Now contemplate they’re seeking to transfer as much as a bigger residence to accommodate a rising household.

The asking worth is $850,000 and the mortgage fee is 6.5%. In the event that they put down 20%, a $680,000 mortgage quantity at 6.5% prices almost $4,300.

We’re speaking a near-200% improve in mortgage fee. And this isn’t an unusual state of affairs.

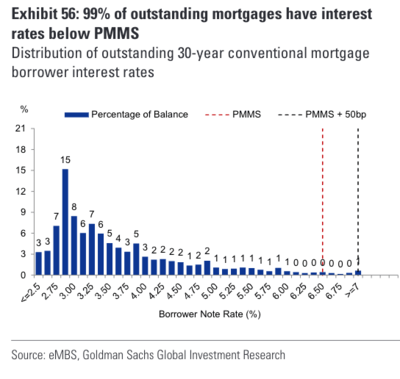

99% of Debtors Now Maintain Mortgage Charges Under Market Charges

A brand new chart has been circulating from Goldman Sachs that reveals 99% of excellent mortgages are priced beneath Freddie Mac’s weekly survey fee.

That survey fee was 6.65% ultimately look, which means just about all present owners have mortgage charges beneath that.

For those who look at it carefully, 28% of present homeowners have a fee beneath 3%, and one other 44% have charges beneath 4%.

That’s 72% of present properties with a mortgage priced beneath 4%. You anticipate them to commerce that for a 6.5% and even 7% mortgage fee?

For 99% of present owners with a mortgage, there’s little incentive (or need) to maneuver from a mortgage financing standpoint.

Positive, some conditions might warrant a transfer, and roughly 42% of houses within the U.S. are owned free and clear (no residence mortgage connected).

However this paints a really completely different housing market than the one seen again in 2007.

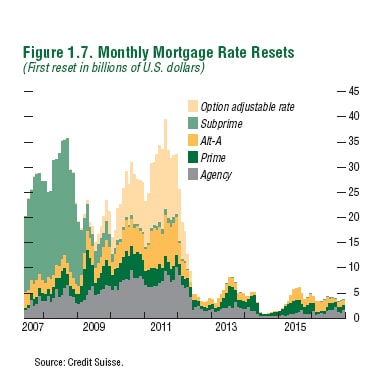

Owners Couldn’t Afford to Keep in 2007

Again in the course of the Nice Recession housing market, one other chart was circulating, and it regarded nothing like the present one. The truth is, it was fairly the other.

It displayed the lots of of billions in adjustable-rate mortgages (ARMs) that have been attributable to reset in coming months and years.

By reset, I imply regulate a lot greater, both to a fully-amortizing fee from detrimental amortization (or from interest-only).

Or those who have been merely adjusting to the fully-indexed fee after the preliminary teaser fee was exhausted.

In both case, the fee was anticipated to rise considerably, probably resulting in fee shock. And extra importantly, an unaffordable mortgage.

And keep in mind, many of those owners weren’t correctly certified for a mortgage to start with.

Included within the chart have been possibility ARMs, subprime loans, Alt-A mortgages, and commonplace prime and company stuff.

The chart was terrifying and mainly summed up the unsustainable housing market in a single easy graph. In these days, owners couldn’t afford to remain.

So for these trying to attract parallels between from time to time, you would possibly need to evaluation the 2 charts aspect by aspect.

Positive, residence costs are inflated in the intervening time, and mortgage charges are dear. But it surely’s simply not the identical housing market.

Sure, one thing has to offer, however I don’t know if present owners are going to be giving up their sub-4% mortgage fee.

What we’d like for a wholesome housing market is long-term fastened mortgage charges again within the 4-5% vary.

This could be useful for brand spanking new patrons, present owners seeking to transfer, and even the Fed!

[ad_2]