[ad_1]

After the Price range 2023, what are the NPS Tax Advantages 2023 underneath the brand new tax and previous tax regimes? This confusion began primarily as a result of the federal government confused selling the brand new tax regime relatively than the previous one. Therefore, allow us to perceive the NPS tax advantages in each regimes intimately.

All of you understand that in the course of the Price range 2020, the Authorities launched a brand new tax regime. Additionally, the Authorities gave you the choice to decide on both the previous tax regime or the brand new tax regime.

Nevertheless, in case you attempt to decide on the brand new tax regime, then you must overlook sure deductions and exemptions. I’ve written an in depth put up on this. You may check with the identical “New Tax Regime – Full listing of exemptions and deductions not allowed“.

Due to these modifications, many people have been confused about what would be the NPS Tax Advantages 2023.

NPS Tax Advantages 2023 – Beneath New Tax and Previous Tax Regimes

Now allow us to perceive the assorted taxation points with respect to NPS.

1. NPS Tax Advantages whereas investing

First, allow us to perceive the NPS Tax advantages you’re going to get on the time of investing. As a consequence of Price range 2020, right here the large modifications occurred and therefore allow us to perceive what are the tax advantages in case you opted for an previous tax regime and what in case you opted for the brand new tax regime.

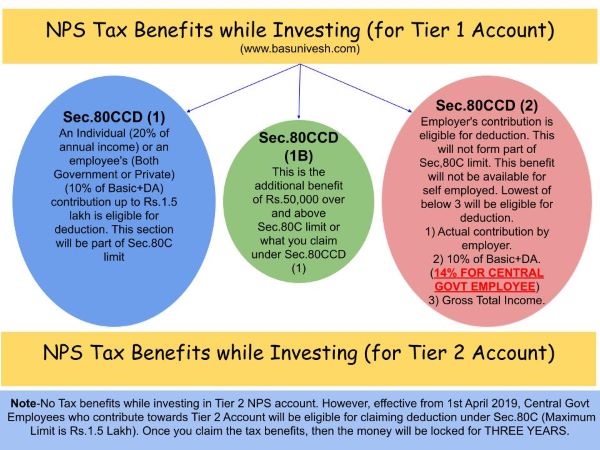

# NPS Tax Advantages 2023 underneath the previous tax regime – Tier 1

Should you want to retain the previous tax regime in your IT return submitting, then the previous taxation guidelines with respect to NPS will proceed as traditional.

I attempted to elucidate the identical from the beneath picture. Do not forget that tax advantages underneath Tier 1 and Tier 2 aren’t obtainable for all buyers. Tier 2 tax advantages can be found just for Authorities Staff.

Allow us to focus on one after the other as beneath.

NPS Tax Advantages underneath Sec.80CCD (1)

- The utmost profit obtainable is Rs.1.5 lakh (together with the Sec.80C restrict).

- A person’s most 20% of annual revenue (Earlier it was 10% however after Price range 2017, it elevated to twenty%) or an worker’s (10% of Fundamental+DA) contribution will probably be eligible for deduction.

- As I mentioned above, this part will type the a part of Sec.80C restrict.

NPS Tax Advantages underneath Sec.80CCD (2)

- There’s a false impression amongst many who there isn’t any higher restrict for this part. Nevertheless, the restrict is the least of the three situations. 1) Quantity contributed by an employer, 2) 10% of Fundamental+DA (For Central Authorities Staff it’s now 14% of Fundamental+DA efficient from 1st April 2019), and three) Gross Whole Revenue.

- That is an extra deduction that won’t type the a part of Sec.80C restrict.

- The deduction underneath this part is not going to be eligible for self-employed.

Additionally, in case your employer contribution underneath Sec.80CCD(2) is greater than Rs.7,50,000 a 12 months (together with EPF and Superannuation), then such exceeded contribution will probably be taxable revenue within the palms of the worker.

In truth, even the returns on the such exceeding quantity of Rs.7,50,000 (from NPS, EPF, and Superannuation) will probably be taxable annually.

NPS Tax Advantages underneath Sec.80CCD (1B)

- That is the extra tax advantage of as much as Rs.50,000 eligible for an revenue tax deduction and was launched within the Budger 2015

- Launched in Price range 2015. One can avail of the advantage of this Sect.80CCD (1B) from FY 2015-16.

- Each self-employed and staff are eligible for availing of this deduction.

- That is over and above Sec.80CCD (1).

# NPS Tax Advantages 2023 underneath the previous tax regime – Tier 2

Earlier there was no revenue tax profit in case you put money into a Tier 2 Account. Nevertheless, the Authorities of India modified the principles not too long ago. In line with this, if Central Authorities Worker contributes in the direction of a Tier 2 Account, then he can declare the tax advantages underneath Sec.80C (The mixed most restrict underneath Sec.80C will probably be Rs.1.5 lakh ONLY). Additionally, if somebody availed of such tax advantages, then the invested cash will probably be locked for 3 years (precisely like ELSS Mutual Funds).

# NPS Tax Advantages 2023 underneath the brand new tax regime – Tier 1

Should you adopted the brand new tax regime, then as I discussed in my older put up ” New Tax Regime – Full listing of exemptions and deductions not allowed“, you must overlook the tax advantages which you’re availing underneath Sec.80C.

Therefore, clearly, the NPS Tax Advantages 2023 underneath Sec.80C, Sec.80CCD(1), and Sec.80CCD(1B) is not going to be obtainable for you. As a result of Sec.80CCD(1) and Sec.80CCD(1B) are a part of the Sec.80C restrict.

Nevertheless, regardless of the employer contribution underneath Sec.80CCD(2) is eligible for deduction underneath the brand new tax regime additionally.

# NPS Tax Advantages 2023 underneath the brand new tax regime – Tier 2

Earlier there was no revenue tax profit in case you put money into a Tier 2 Account. Nevertheless, as a result of Authorities of India modified guidelines, if Central Authorities Worker contributes to a Tier 2 Account, then he can declare the tax advantages underneath Sec.80C (The mixed most restrict underneath Sec.80C will probably be Rs.1.5 lakh ONLY). Additionally, if somebody availed of such tax advantages, then the invested cash will probably be locked for 3 years (precisely like ELSS Mutual Funds).

Nevertheless, underneath the brand new tax regime, you aren’t eligible for tax deduction underneath Sec.80C, there isn’t any tax profit in case you put money into NPS Tier 2 Account.

2. NPS Tax Advantages whereas withdrawing

As soon as attaining the age of 60 or superannuation underneath part 80CCD(5), lumpsum withdrawal of 60% of amassed pension wealth is tax-free. Nevertheless, you must purchase an annuity from the remaining 40%. This will probably be taxed as per your tax slab.

Assume that you simply amassed Rs.100. On this, you must purchase an annuity for Rs.40 from Life Insurance coverage Corporations. They may pay you the pension as per the choice you’ve chosen. This pension is taxable as per your revenue tax slab.

Now the remaining Rs.60 is totally Tax-Free.

Observe-As per Price range 2017, the subscriber whose NPS account is not less than 10 years previous will probably be eligible for withdrawing 25% of his/her contributions (with out accrued revenue earned thereon). This 25% withdrawal will probably be a part of a complete 60% withdrawal (which is tax-free).

3. NPS Tax Advantages on Pre-mature withdrawal

On this case, you’re allowed to purchase an annuity product from 80% of the amassed corpus. So there isn’t any confusion right here because the annuity will probably be taxable revenue for you 12 months on 12 months.

The confusion is about 20% lump sum withdrawal. IT Division wants to come back out with readability. The foundations simply say 40% of lump sum withdrawal from NPS is tax-free. Nevertheless, on this specific case, the lump sum funding is 20%.

Therefore, whether or not the entire 20% is tax-free (as it’s lower than 40% tax-free restrict) or 40% of 20% is simply tax-free (i.e. 8% from 20%). As of now, there isn’t any readability on this side.

4. NPS Tax Advantages on Pre-mature withdrawal

Partial withdrawal from NPS is allowed on sure situations. I defined the identical in my put up “Newest NPS Withdrawal Guidelines 2018“.

There isn’t a readability concerning the tax therapy regarding this partial withdrawal. Nevertheless, I really feel such partial withdrawal will probably be taxed within the 12 months of withdrawal as per the subscriber’s revenue tax slab.

5. NPS Tax Advantages on Pre-mature withdrawal

Authorities Staff-Nominee will probably be allowed to withdraw solely 20% of a lump sum. The nominee should buy the annuity from the remaining 80%. Nevertheless, in case the amassed corpus is lower than or equal to Rs.2,00,000 then his partner (or nominee) can withdraw all the quantity directly with none obligatory.

For others-Nominee will probably be allowed to withdraw 100% amassed corpus. Nevertheless, the nominee has a alternative to purchase an annuity too.

The lump-sum withdrawal by the nominee will probably be exempt from Revenue Tax. If the nominee opted for getting an annuity, then annuity revenue will probably be taxed as per the nominee’s revenue tax slab within the 12 months of receipt.

6. NPS Tax Advantages from Tier 2 Accounts withdrawal

Sadly there isn’t any readability on this side. Few argue that because the construction of Tier 2 is like Mutual Funds, we are able to pay the tax like mutual funds (debt and fairness) primarily based on our holding proportion (both fairness or debt).

Nevertheless, few argue that as within the case of the NPS Tier 2 Account, we’re not paying any STT (Safety Transaction Tax), we should not contemplate the taxation of Tier 2 account as like Mutual funds and needs to be taxed underneath the top of “Revenue From Different Sources”. Additionally, as of now, the NPS Tier 2 account shouldn’t be certified as Capital Asset underneath Part 2.

Personally, I really feel the second opinion of contemplating this as revenue from different sources seems like a sound purpose. Nevertheless, it should not be thought of a rule. I’m simply airing my views. I do know that my view could also be harsh. Nevertheless, so long as there isn’t any readability from IT Division, it’s laborious to guage.

[ad_2]